Predictable. You can’t make predictions. You can’t time the market.

Last week, AI stock madness was all over.

Today it’s back on.

South Korea was up 18% yesterday. Samsung and SK Hynix.

Here’s Jim Cramer from last night:

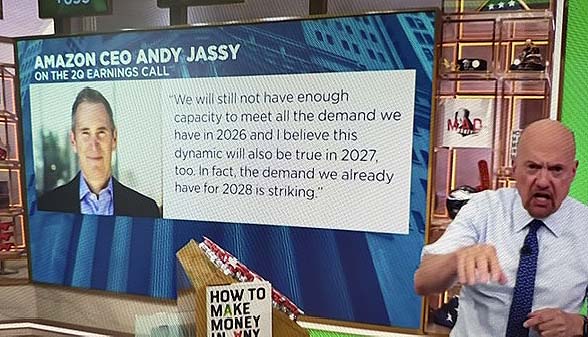

The tech sector has found its savior and his name is Andy Jassy, Amazon CEO. Last week on his conference call he patiently explained the economics of the data center and how patient shareholders could be rewarded with a huge return. One that might happen sooner than you think.

Until Jassy spoke, the markets seemed highly skeptical of how the tech copanies were spending their money.

Because of him. I don’t think that’s any longer the case. …Regular viewers of this show or anyone would know that I’ve been waiting months for Amazon to give us a line of sight. That would be something that can justify why they’re spending so much money on all these data centers. Amazon is a large position in my charitable trust so I wanna know if there’s really a pot of gold at the end of the rainbow.

I think I finally got that answer.

Jassy said at this level of spend and higher we have clear line of sight. All the money we are putting into the data center may not be even enough to capitalize on the opportunity.

Here’s my favorite ETF called VGT compared to Nasdaq and the S&P 500 for this year.

The moral of this chart: If you have a job (i.e. other things to do), put all your money into VGT.

Products and Services I like

+ Mint Mobile.

+ Starlink. My friend used it on his sailing boat (aka) yacht between San Fran and Hawaii. Worked perfectly. I’ve used it in rural Montana. Worked perfectly.

+ Go to iron pots and pans. Give up your nonstick pans, both teflon and ceramic. NYT Wirecutter has reasons.

+ Fidelity’s Active Trader Pro (old version).

+ Lenovo’s X1 Carbon laptop. They give reliability a whole new meaning. Buy from Discount Electronics. Click here.

+ Flaygo $99.97 hearing aids. Click here.

+ Sennheiser headphones for listening to TV.

+ Cortizone-10 anti-itch cream. Actually works.

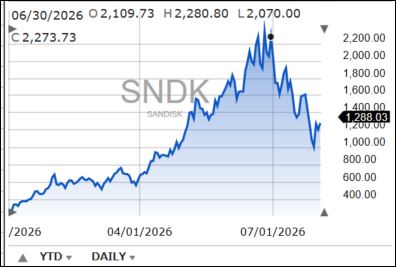

+ SanDisk 512GB Ultra Fit USB 3.2 Gen 1 Flash Drive. $79.99. It’s that little thing sticking out of the laptop’s USB port.

Interestingly, that little backup memory thingee has exactly doubled in price since I last bought it in November 2025. That tells you something. To buy before the price goes up even more, click here.

SanDisk year to date:

Memory has gone mad. SanDisk is up 8% today.

Ripped off by Delta

I changed my fully-refundable ticket business class tickets by two days. Delta hit me for thousands of dollars.

Moral: Don’t change close to departure.

I asked Google’s Gemini (whom I love)

+ Is there a cheap time to buy a airline ticket?

Yes, cheap times to buy airline tickets include booking 1 to 3 months before domestic flights (2 to 8 months for international), flying on Tuesdays and Wednesdays, and traveling during off-peak shoulder seasons.

+ Domestic flights: Book 1 to 3 months in advance.

+ International flights: Book 2 to 8 months in advance.

- Last-minute windows: Avoid booking within 14 days of departure when prices spike.

- Cheapest days: Tuesdays and Wednesdays usually have lower passenger demand.

- Expensive days: Fridays and Sundays cost the most because of weekend trips.

Off-peak months: January, February, September, and October offer lower prices.

Airline tips (from Harry):

+ Go to Europe business class. Come back cheaper premium economy. It’s a day flight. you don’t need lie-flat.

+ Never check luggage.

+ Sitting in an aisle seat? Don’t let them open the overhead bin with you sitting underneath it. A friend got knocked unconscious when a pair of heavy ski boots fell and hit her. She still hasn’t recovered.

+ Airline web sites suck. Going different places? Delta has one-way, return and “multicity.” Saves big over booking two tickets.

+ Duxiana makes the best travel pillow. I never travel without my Duxiana.

I am obsessed with type sizes and faces

I send emails in 14pt Verdana, which is sans serif. . I get many emails in tiny 8pt. To read I go to Other Actions/Options/Zoom and increase it to 200%. Outlook offers that.

Which brings me to this email. I can send it out in any which way. But how you get it depends on your own email client. There’s no standard – unlike the Internet which has Ethernet, HTML, jpeg, etc.

In short, if you can’t read an email you just received (from me, or others), here are your options:

+ Go to the web site.

+ Zoom it up, if your email client has that option.

+ Forward the email to yourself in bigger type.

+ Buy stronger reading glasses.

+ Junk this article. You can read and hear fine. And you don’t need advice from the likes of crabby old men, who think they’re funny, or worse, still useful.

I do like Instagram

My feeds include tennis, mammals in Africa or “research.” I now know how to be happy. I don’t own Meta, which owns Instagram.

Favorite quote

“We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.” — Roy Amara.

Upping

Well, we upped the type size on this email. Let me know if it works better for you.

We had oodles of rain. Flooded everyone. And doubled my grass cutting bill.

Off to play tennis. See you very soon. — Harry Newton