So many dumb things in finance — Part 1

Money management, also called “finance,” attracts some of the dumbest people. There are three reasons:

1. The enormous fees. Especially if you have lots of money “under management.” Once you have your client’s money, you can easily deduct your fees. You don’t have to send them a bill. They don’t freak when they see it on their Visa. Or see the precipitous drop in their bank account. The fees are absorbed by the balance of money “under management.”

2. You’re generally doing good for your client — because the market goes up most years. You won’t be number one performer. There’s only one of them. But, so long as your performance is more than your fees, you’ll keep your client and, most importantly, the fees. Clients are sticky.

3. Managing money involves little effort analyzing stocks. In fact, you don’t have to do any analyzing. Waste of time. Buy what’s in one or two index funds works just fine. Most of your real work is marketing — attracting money to “manage.” There are a million ways of doing that none of which are very clever. Just tune into CNBC. The ads have gorgeous scenery and creative graphics — but never any useful information — like the manager/fund’s performance. All ad agencies can deliver gorgeous animation up the ying yang, up the wazoo as well. You can also get free marketing. Be a guest on CNBC, or Bloomberg. Become a talking head. You job is to burble the conventional wisdom of the day. You don’t have to tell anyone to sell their stocks — though that’s what most investors should have done a a year ago. You need to prattle on about the reasons for buying/owning a hot stock. You can find all the material you want on the company’s web site. Check out Nvidia’s web site. It’s classic technology hype. It suckered me in.

So many dumb things in finance — Part 2

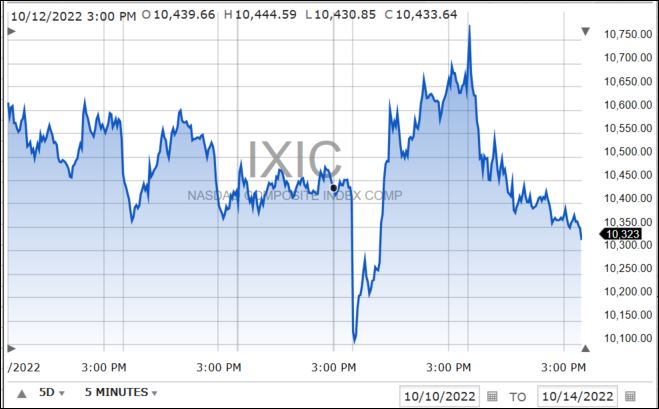

You can make a fortune, if you short the English pound at the right time. Like George Soros did. You can do what happened last week.

That huge drop and then a huge bounce-back was a classic short squeeze that killed a whole bunch of hedge funds and “investors” who had bought oodles of PUTs. They got squeezed by machines buying.

+ Pension funds guarantee a percentage return to their pensioners. Some years (like this one) they earn less than what they guaranteed. There’ll be a shortfall. Where do they get the shortfall from? The government? Their pensioners? From me? From you? Or they just issue a public statement, “Oops!” Or they close their doors, as some will. Pity poor retired teachers.

+ Hedge funds don’t hedge. They promise to hedge, i.e. reduce the risk. But then, the managers get carried away with some momentary insanity — for example, pandemic stocks, like Peloton, Zoom or DocuSign. They load up the boat. They forget to sell or hedge.

+ Overseas countries borrow money and promise to repay their borrowings in U.S. dollars. They figure they’ll earn money in their local currency, which will stay with the dollar. Which it often doesn’t. It often depreciates. Since the recent huge rise in the value of the U.S. dollar, there are dozens of countries who can’t pay their dollar-denominated loans back. Turkey is one.

+ Hedge funds buy stocks on margins. Like huge margins — sometimes over 90%. A small drop in the value of their holdings means the margin lender will sell the losing stocks. If that doesn’t pay off the loan, they will sell your good stocks. Then your portfolio will really take a hit. If there’s enough money at stake, it can bring down the entire financial system, as nearly happened with Long Term Capital Management in 1998.

+ Many investors thought bonds were safe. As they got older, they bought more of them. That was conventional wisdom. Everyone’s heard of the 60-40 rule or the 40-60. It shows what percentage should be in bonds and what in equities. Older people bought long-term bonds, thinking they were safer than stocks. But bonds are only safe if you hold them until their maturity. But who’s going to be around for the maturity of a 30-year bond — not me. No matter how much tennis I play. Delicious thought: If I did live that long, I’d be the oldest person on the planet. And they’d study my thoughts, i.e. these ones.

Priceless comments on our daily life

I pick cartoons that make me laugh. Sometimes one cartoon makes me laugh for days. It keeps popping into my tiny brain.

For example:

Congratulations to President Xi

President Xi is now President for Life. My heart goes out to the Chinese people suffering his increasing insanity. Let’s start with covid lockdowns. He’ll lock 10 million people up in their apartments if there’s half a dozen covid cases. Factories close. Jobs are lost. Kids can’t get educated. And he won’t buy vaccines from Moderna and Pfizer which are far more effective than his home-grown garbage. Why? He’s nuts.

My favorite Xi madness is The App. Every phone in China is meant to have it. You listen to Xi’s thoughts and speeches. You study them. There are quizzes on his thoughts. How long you spend on the site and how you do on the quizzes are noted by a giant database in the cloud that records everything that happens on your cellphone. IF you work for the government — and oodles do — your time on the app and how well you do on the quizzes is passed along to your boss and he/she uses those results to promote, demote or fire you.

I don’t make this stuff up.

If you know anyone who’d like to receive this blog by email, subscribe them at the top left of the web page. Click here. Or send me an email.

See you shortly. — Harry Newton